Week of January 31, 2022 in Review

Economists were anticipating 150,000 job creations in January, but job growth came in well above these expectations per the Bureau of Labor Statistics (BLS), which reported 467,000 new jobs. In addition, there were positive revisions to the data for November and December adding 709,000 new jobs in those months combined, making last week’s report even stronger.

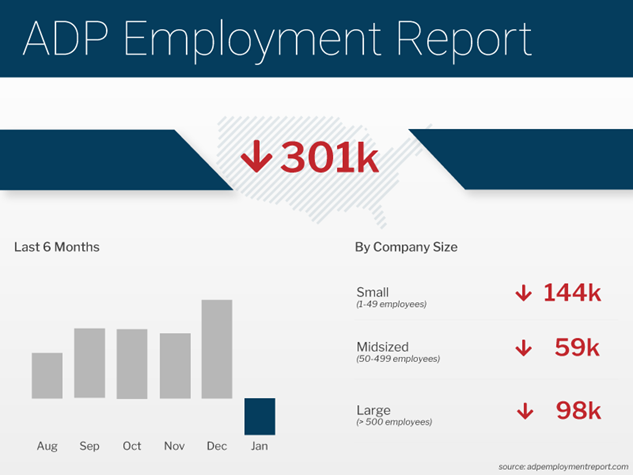

However, private sector payrolls missed expectations in January, with the ADP Employment Report showing that there were 301,000 job losses – well below the 200,000 job gains that were expected. Losses were reported across all sizes of businesses, with the majority in small businesses. Part of the miss has to do with when Omicron cases peaked and how this data is collected, as explained below.

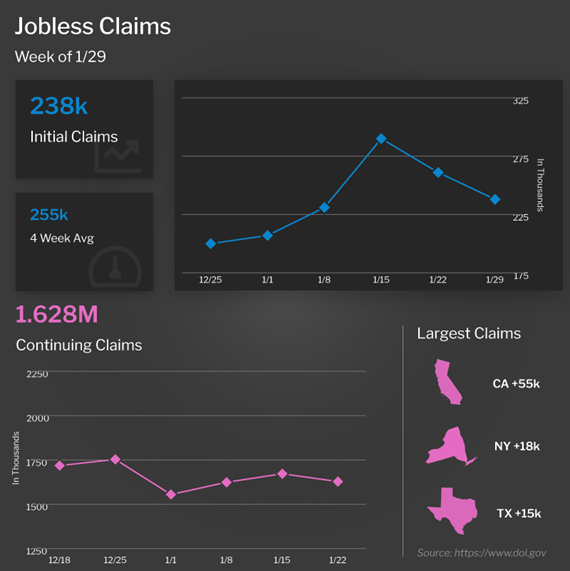

After the recent rise in jobless claims, likely due to the rise in Omicron cases, Initial and Continuing Claims both declined in the latest week as Omicron cases are slowing down. There are now 2.067 million people in total receiving benefits, which is a stark contract to the 18.5 million people receiving benefits in the comparable week the previous year. Claims are at very strong pre-pandemic levels, showing that the labor market remains tight.

The JOLTS (Job Openings and Labor Turnover Survey) report showed that there were almost 11 million job openings in December, which is near the record high of almost 11.1 million reported last July. While Omicron certainly could have impacted this data, it is also not surprising, as many companies have expressed a need for more workers.

In housing news, CoreLogic’s Home Price Index report for December showed that home prices rose by 1.3% from November and 18.5% year over year. This annual reading is an acceleration from 18% in November and is the highest reading in the 45-year history of the index.

Meanwhile, Apartment List’s National Rent Report showed that rents also rose 0.2% in January and almost 18% year over year. To put this in context, annual rent growth averaged just 2.3% in the pre-pandemic years from 2017-2019. Over the last four months, rents are up about 1% and while the rise in rents is slowing, this could be due to some seasonal factors. It is possible that higher rent growth may return as more people move once the weather warms.

Lastly, the Fed’s actions remain crucial to monitor in the months to come, as they will play an important role in the direction of the markets and mortgage rates this year. Don’t miss our important breakdown on what’s happened in past cycles and what to look out for ahead.

January Job Creations Beat Expectations

The Bureau of Labor Statistics (BLS) reported that there were 467,000 jobs created in January, which was much more than expectations of 150,000. In addition, there were positive revisions to the data for November and December adding 709,000 new jobs in those months combined, making last week’s report even stronger.

Note that there are two reports within the Jobs Report and there is a fundamental difference between them. The Business Survey is where the headline job number comes from and it’s based predominately on modeling.

The Household Survey, where the Unemployment Rate comes from, is done by actual phone calls to 60,000 homes. The Household Survey also has a job loss or creation component, and it showed there were 1.2 million job creations, while the labor force increased by 1.39 million. The number of unemployed people increased by 194,000, causing the unemployment rate to increase slightly from 3.9% to 4%.

The U-6 all-in unemployment rate, which is more indicative of the true unemployment rate, improved from 7.3% to 7.1%, meaning it is almost back at the levels we saw in February 2020 before the pandemic began.

Average hourly earnings rose by 0.7% in January and are up 5.7% year over year, which is a full percentage point higher than the previous reading. Average weekly earnings were only up slightly on a monthly basis due to less hours being worked, which is likely due to Omicron’s impact. On an annual basis, they were up 4.2%.

Private Payrolls Drop in January

The ADP Employment report, which measures private sector payrolls, showed that there were 301,000 job losses in January – well below the 200,000 job gains that were expected. December’s figures were also revised slightly lower from 807,000 to 776,000 new jobs in that month.

Job losses were reported across all sizes of businesses, with the majority of those reported at small businesses. Small businesses (1-49 employees) lost 144,000 jobs, mid-sized businesses (50-499 employees) lost 59,000 jobs, and large businesses (500 or more employees) lost 98,000 jobs.

To understand the miss in this data, it’s important to look at how it’s collected. Over 14 million workers missed work at some time during January due to Omicron. If they were not working and not receiving paid sick leave during the sample week in which the data was collected, those workers were not counted as employed.

The sample week was the week that included January 12 and the peak of Omicron cases was January 11. And since most of the job losses came from small businesses, particularly those with 1-19 employees (-106,000 jobs), there is a good chance many of those businesses were not paying sick leave.

Initial and Continuing Jobless Claims Decline

The number of people filing for unemployment benefits for the first time fell by 23,000 in the latest week, with Initial Jobless Claims reported at 238,000. Continuing Claims, which measure people who continue to receive benefits after their initial claim is filed, also fell 44,000 to 1.63 million.

After the recent rise in jobless claims, which was likely due to the rise in Omicron cases, claims are now falling once again as Omicron cases are slowing down.

There are now 2.067 million people in total receiving benefits, which is a decline from 2.14 million in the prior week and a stark contract to the 18.5 million people receiving benefits in the comparable week the previous year. Claims are at very strong pre-pandemic levels, showing that the labor market remains tight.

Home Price Appreciation Reaches New High

CoreLogic released their Home Price Index report for December, showing that home prices rose by 1.3% from November and 18.5% year over year. This annual reading is an acceleration from 18% in November and is the highest reading in the 45-year history of the index.

Within the report, the hottest markets remained Phoenix (+30%), Las Vegas (+24%), and San Diego (+22%).

CoreLogic forecasts that home prices will remain flat in January and appreciate 3.5% in the year going forward. Yet, they remain conservative in their forecasting and continue to miss forecasts by a large margin.

For example, CoreLogic had forecasted prices would remain flat from November to December, and they actually rose 1.3%. And when we look to their report for December 2020, they forecasted that home prices would increase 2.5% annually – and yet they reported today that prices rose 18.5%.

Apartment List’s National Rent Report showed that rents also rose 0.2% in January and almost 18% year over year. To put this in context, annual rent growth averaged just 2.3% in the pre-pandemic years from 2017-2019. Over the last four months, rents are up about 1%. While the rise in rents is slowing, this could be due to some seasonal factors and it is possible that higher rent growth may return as more people move once the weather warms.

What to Look for From the Fed in the Months Ahead

The Fed’s actions remain crucial to monitor in the months to come, as they will play an important role in the direction of the markets and mortgage rates this year.

Note that the Fed has two levers they can pull for tightening the economy – hiking their benchmark Fed Funds Rate and reducing their balance sheet. The Fed Funds Rate is the interest rate for overnight borrowing for banks and it is not the same as mortgage rates.

Hiking the Fed Funds Rate will actually be a good thing for mortgage rates, as the Fed curbs inflation and preserves the fixed return a longer data Bond provides. However, reducing their balance sheet (which means allowing Bonds to fall off their balance sheet and no longer reinvesting in them each month) would cause more supply on the market that has to be absorbed. This can cause mortgage rates to move higher.

Looking at past cycles, when the Fed began hiking the Fed Funds Rate in December 2015, mortgage rates moved lower. They waited a full year until the next hike, and during that time, inflation rose and mortgage rates moved higher. When they hiked again in December 2016, mortgage rates moved lower as inflation was put in check.

In October 2017, the Fed announced that they would start to allow their balance sheet to runoff and we saw mortgage rates move higher in response. When they began to slow the runoff in March 2019, mortgage rates moved lower and then really started to move down in July when the Fed ended the runoff altogether and started reinvesting in MBS and Treasuries.

Again, the point here is that mortgage rates like when the Fed hikes the Fed Funds Rate and hate when they reduce their balance sheet. We saw some of this dynamic last week when the Bank of England announced they were starting the runoff of their balance sheet, noting that by the end of 2023 they will not just stop reinvestments, they will be outright sellers of Bonds. Global yields can impact our yields and Mortgage Bonds did not react favorably to the news when it was announced.

The bottom line is that we will want to closely watch how the Fed tries to walk the tightrope of hiking and allowing runoff during 2022.

Family Hack of the Week

You’ll score extra points with these crowd-pleasing Classic Buffalo Wings from our friends at Delish, perfect for game day or any favorite celebration!

Preheat oven to 400 degrees Fahrenheit and place a wire rack over a baking sheet. In a large bowl, toss two pounds of chicken wings with two tablespoons vegetable oil, 1 teaspoon garlic powder, Kosher salt and black pepper.

Place on prepared baking sheet and bake until chicken is golden and skin is crispy, approximately 50 to 60 minutes, flipping the wings midway through.

While wings are baking, whisk together 1/4 cup hot sauce and 2 tablespoons honey. Once simmering, stir in 4 tablespoons butter. Cook until butter is melted and slightly reduced, about 2 minutes.

Heat broiler on low. Transfer baked wings to a bowl and toss with buffalo sauce, coating completely. Return wings to rack and broil until sauce caramelizes, 3 minutes, watching them carefully.

Enjoy with classics like Ranch dressing, carrot and celery sticks!

What to Look for This Week

The week kicks off on Tuesday with an update on how small businesses are feeling when the National Federation of Independent Business Small Business Optimism Index for January is reported.

Thursday brings a crucial update on inflation with January’s Consumer Price Index along with the latest Jobless Claims figures.

Investors will also be closely watching Wednesday’s 10-year Note and Thursday’s 30-year Bond auctions for the level of demand.

Technical Picture

Mortgage Bonds broke below the well-defined range they had been trading in, falling beneath the floor at 101.578. They went all the way down to the next floor at 101 but bounced higher from it. The 10-year ended last week trading at around 1.91% – you have to go back around 2.5 years to see yields meaningfully above these levels.