Week of November 15, 2021 in Review

Home construction was certainly impacted in October by the aforementioned shortages, as Housing Starts fell 0.7% from September. More importantly, starts for single-family homes declined 3.9% and they were also down almost 11% year over year.

Building Permits, which are a good forward-looking indicator of construction, were up 4% in October. Permits for single-family homes rose 2.7% in October but they were down 6.3% year over year.

Yet, builders remain confident due in large part to the high demand for homes around the country. The National Association of Home Builders (NAHB) Housing Market Index, which is a real-time read on builder confidence, rose 3 points to 83 in November. This is the largest monthly increase since February and marks three consecutive months of increases. Any reading over 50 on this index, which runs from 0 to 100, signals expansion.

Consumer confidence fell to the lowest level in 10 years this month, per the University of Michigan’s Consumer Sentiment Index. Of note, those who said it’s a good time to buy a home declined to the lowest level since 1982. However, while it may not be an easy time to buy a home, demand for homes remains strong, especially given the increases in rent that have been reported.

CoreLogic released their single-family rental index, showing that rents are up over 10% year-over-year to the highest reading in 16 years. Attached rentals were up almost 8%, while detached and with more space were up over 12%.

There was some good news from the labor sector, as Initial and Continuing Jobless Claims both declined in the latest week, to 268,000 and 2.08 million respectively. This data represents new pandemic-era lows. Yet, even with this decline in people filing for unemployment benefits, job openings remain extremely elevated, as highlighted below.

Despite the rise in inflation we have seen, there were strong reports from the manufacturing sector. The Empire State Index, which shows the health of manufacturing in the New York region, came in above expectations in November while the Philadelphia Fed Index surged to a 7-month high. Retailers also had reason to smile as Retail Sales beat expectations in October, up 1.7% from September, even in the face of higher prices for many items.

Lastly, President Biden signed a $1.2 trillion bipartisan infrastructure bill into law, which includes $550 billion in new spending on our nation’s roads, bridges, ports, water and rail. It also provides $65 billion to expand broadband infrastructure and $55 billion for clearwater investments. Unlike other bills, this bill will go into effect over the next 5 years rather than all at once.

Builder Confidence Increases for Third Month In a Row

The National Association of Home Builders Housing Market Index, which is a real-time read on builder confidence, rose 3 points to 83 in November. This is the largest monthly increase since February and marks three consecutive months of increases.

Looking at the components of the index, current sales conditions rose 3 points to 89, sales expectations for the next six months were unchanged at 84, and buyer traffic rose 3 points to 68

Any reading over 50 on this index, which runs from 0 to 100, signals expansion. Despite the supply-side challenges and lot and labor shortages builders are facing, confidence has risen this fall due to the continued high demand for homes around the country.

Decline in Housing Starts Hurts Already Low Inventory

Housing Starts, which measure the start of construction on homes, fell once again in October, as they were reported down 0.7% at a 1.53 million unit annualized pace. Starts were nearly flat compared to October of last year, up just 0.4%.

Starts for single-family homes, which are in such high demand, also declined 3.9% from September to a 1.04 million unit pace. They were also down almost 11% year over year. The only area that saw an increase in Starts was in buildings with 5 or more units.

The previously mentioned supply, labor and lot shortages are hindering builders from completing the level of homes needed to help with the inventory shortages many buyers have experienced around the country. This should continue to contribute to a tight inventory landscape into the foreseeable future.

There was some better news regarding future construction, as Building Permits (which are a good forward-looking indicator of future supply) were up 4% from September to October and 3.4% versus October of last year. Permits for single-family homes rose 2.7% in October but they were down 6.3% year over year.

Housing units that are authorized but not started continue to rise, showing that the backlog of homes is growing, unfortunately. It grew almost 5% in October to 265,000 units not started and this category is now up almost 45% compared to October of last year.

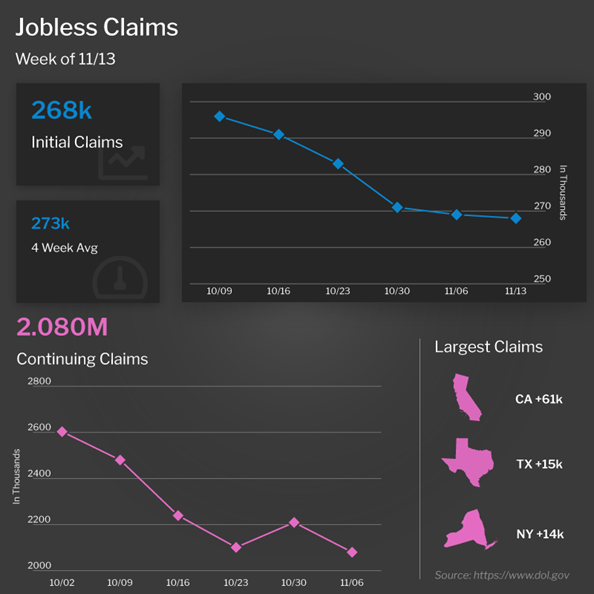

Jobless Claims Hit New Pandemic-Era Lows

The number of people filing for unemployment benefits for the first time fell by 1,000 in the latest week, as Initial Jobless Claims dropped from 269,000 to 268,000. Continuing Claims, which measures individuals who continue to receive benefits, decreased by 129,000 to 2.08 million. Both of these figures are at pandemic-era lows and also at levels that were more normal prior to the pandemic.

Despite the decline in jobless claims, job openings remain at elevated levels. The Jolts (Job Openings and Labor Turnover) survey showed there were 10.4 million job openings at the end of September. While this is a decline from the levels reported at the end of July and August, the bottom line is that record levels of people are quitting their jobs. In September, 164,000 people quit their jobs, bringing the total to an all-time high of 4.434 million over the last 12 months. This is up 34% year over year.

On a related note, the Atlanta Fed’s wage growth tracker showed that wages are up 4.1% year over year in October, which is near the highest level in 13 years. Remember, wage-pressured inflation like this tends to be much stickier.

A Note About Consumer Confidence and Rents

Consumer confidence fell to the lowest level in 10 years this month, per the University of Michigan’s Consumer Sentiment Index. Inflation is surging, reducing living standards, and those surveyed don’t think that the Fed’s policy is doing anything to help.

Of note, those who said it’s a good time to buy a vehicle fell to the lowest level since 1978 while those wanting to buy a major household item fell to the lowest reading since 1980.

As for those who said it’s a good time to buy a home, that declined to the lowest level since 1982. However, while it may not be an easy time to buy a home, demand for homes remains strong, especially given the increases in rent that have been reported.

CoreLogic released their single-family rental index, showing that rents are up over 10% year-over-year to the highest reading in 16 years. Attached rentals were up almost 8%, while detached and with more space were up over 12%.

While this headline figure is elevated, it is lower than Apartment List’s reading that rents are up 16.4% year-to-date. Note that the main difference between these reports is that CoreLogic takes all rents including renewals into account, while Apartment List’s calculation just factors in new rents.

In both cases, these metrics are much higher than October’s Consumer Price Index rental component, which showed only a 2.7% increase. It just goes to show how understated inflation is within the CPI, as its rental component is out of touch with every other metric.

Family Hack of the Week

Deciding what to do with Thanksgiving leftovers is easy thanks to this Leftover Turkey Soup recipe, courtesy of our friends at Taste of Home.

Add leftover turkey carcass, 3 quarts of water and 2 cans (14-1/2 ounces each) of reduced sodium chicken broth to a stockpot. Bring to a boil, then reduce heat, cover and simmer for 4 to 5 hours.

Remove carcass from stock. Remove any meat, dice and then return to stock along with 1/2 cup uncooked long grain rice, 1 finely chopped medium onion, 4 finely chopped celery stalks, 2 medium carrots (grated), 1 bay leaf and a dash of poultry seasoning. Add onion powder, garlic powder, Kosher salt and pepper to taste.

Cover and simmer over medium-low heat until the rice is cooked. Discard bay leaf.

Enjoy with your favorite crusty bread!

What to Look for This Week

The week kicks off with more housing news on Monday when October’s Existing Home Sales are reported.

Then, a cornucopia of reports will be released on Wednesday ahead of the Thanksgiving holiday, including the latest Jobless Claims figures, the second reading on third quarter GDP, and October readings for Durable Goods, New Home Sales, Personal Income, Personal Spending, and Personal Consumption Expenditures, the latter of which will provide a crucial update on the Fed’s favored inflation measure.

The markets will be closed on Thursday in celebration of Thanksgiving. They will also be closing early on Friday.

Technical Picture

Mortgage Bonds made some initial gains last Friday morning after the news of COVID-related lockdowns in parts of Europe, but they were subsequently rejected by the ceiling at their 25-day Moving Average. They ended last week in a wide range, with the aforementioned ceiling at the 25-day Moving Average and the next level of support down at 102.156. The 10-year has moved lower to around 1.54% and ended the week trading in a range between resistance at the 25-day Moving Average and a floor of support at the 50-day Moving Average at 1.50%.