Week of November 13, 2023 in Review

Inflation continued to cool in October, while we saw an uptick in construction despite dampening homebuilder confidence. Plus, the latest Retail Sales and Jobless Claims suggest a slowing economy. Here are last week’s headlines:

Easing Consumer Inflation a Welcome Sign

October’s Consumer Price Index (CPI) showed that inflation was flat compared to September, with this monthly reading coming in below the consensus estimate of a 0.1% gain. On an annual basis, CPI fell from 3.7% to 3.2%, near the lowest level in more than two years. Core CPI, which strips out volatile food and energy prices, increased 0.2% while the annual reading declined from 4.1% to 4%, reaching a two-year low.

Declining gasoline and used car prices and moderating shelter costs helped keep a lid on inflation last month, even in the face of rising costs for motor vehicle and health insurance.

What’s the bottom line? Inflation has made significant progress lower after peaking last year, with the headline reading now at 3.2% (down from 9.1%) and the core reading at 4% (down from 6.6%). Remember, the Fed has been hiking its benchmark Fed Funds Rate (which is the overnight borrowing rate for banks) to try to slow the economy and curb inflation.

Their latest hike in July was the eleventh since March of last year, pushing the Fed Funds Rate to the highest level in 22 years. The Fed did not hike at their September or November meetings, so they could continue to assess incoming inflation, labor sector and other economic data.

Has there been enough progress for another pause at the Fed’s next meeting? We’ll find out on December 13.

Huge Progress in Wholesale Inflation

The Producer Price Index (PPI), which measures inflation on the wholesale level, fell by 0.5% in October, marking the largest monthly drop since April 2020. On an annual basis, PPI declined from 2.2% all the way down to 1.3%. Core PPI, which also strips out volatile food and energy prices, was flat for the month with the year-over-year reading down from 2.7% to 2.4%. All these numbers were below estimates.

What’s the bottom line? This latest PPI report is another encouraging sign that inflation is easing, with October’s 1.3% year-over-year reading a sharp drop from last year’s 11.7% peak. Plus, PPI tends to lead the way for CPI, which suggests further good progress moving forward.

Are “Better Building Conditions” Ahead?

The National Association of Home Builders (NAHB) Housing Market Index fell six points to 34 in November, keeping builder sentiment below the key breakeven level of 50. This marks the fourth straight monthly decline, as sentiment has fallen 22 points since July, reaching the lowest level since last December.

All three components of the index moved lower, with current sales conditions down six points to 40, future sales expectations dipping five points to 39, and buyer traffic falling five points to 21.

What’s the bottom line? High mortgage rates were a key reason cited for declining builder confidence, yet “recent macroeconomic data point to improving conditions for home construction in the coming months,” per NAHB Chief Economist Robert Dietz. Plus, there was other good news for buyers, as more builders (36%) reported cutting prices, which is the highest percentage in a year.

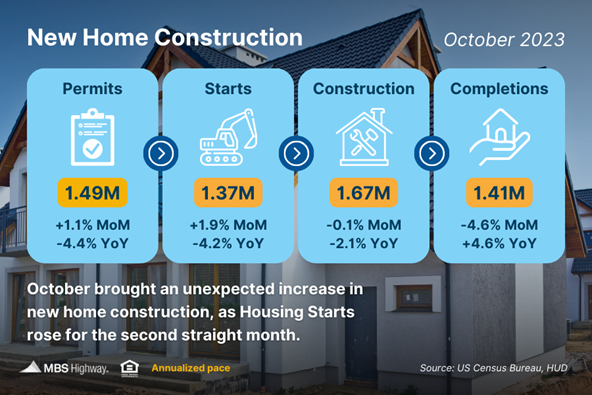

Housing Starts Rise but More Supply Is Needed

Housing Starts (which measure the start of construction on homes) unexpectedly rose in October for the second straight month, up 1.9% from September. While the largest share of the increase came in multi-family units, starts for single-family homes did inch higher by 0.2%. Building Permits, which are indicative of future supply, also rose in October after declining in September. Permits for single-family homes reached their highest level in a year.

What’s the bottom line? Alicia Huey, NAHB Chair, noted that, “Despite higher interest rates in October, the lack of existing home inventory supported demand for new construction in the fall.” Yet, even with the uptick in Housing Starts, more supply is still needed to meet demand.

In fact, when we look at the pace of completed homes that will be coming to market (around 1.41 million homes annualized) and subtract roughly 100,000 homes that need to be replaced every year due to aging, we’re well below demand as measured by household formations that are trending at 2 million. Even looking at future supply (Building Permits at 1.49 million annualized), we’re still much lower than where we need to be.

The bottom line is that more demand than supply will continue to be supportive of home values, especially when we reach the spring homebuying season next year.

Retail Sales Suggest a Slowdown

Retail Sales fell 0.1% in October, marking the first monthly decline since March, albeit a smaller one than economists had forecasted. Sales were up 2.5% when compared to October 2022, but they’re slowing sharply given that sales in September were 4.1% higher than a year earlier.

What’s the bottom line? Retail Sales are clearly trending lower, as they fell 0.1% in October after rising 0.9% in September. Plus, last month’s report showed a clear bias toward spending on non-discretionary items versus discretionary ones, which also suggests an economic slowdown. Again, with the Fed looking for signs that our economy is cooling, will this report help convince members to pause rate hikes once more in December?

Continuing Jobless Claims Hit a Two-Year High

Initial Jobless Claims reached a three-month high, up by 13,000 as 231,000 people filed for unemployment benefits for the first time. What’s more, Continuing Claims increased by 32,000, with 1.865 million people still receiving benefits after filing their initial claim. This is the highest level of Continuing Claims since November 2021.

What’s the bottom line? Initial Jobless Claims remain relatively low on a historical basis, suggesting that employers are trying to hold on to workers, though the number of first-time filers has begun to trend higher in recent weeks. Plus, Continuing Claims have risen for eight straight weeks, up by 207,000 since September, suggesting that it’s becoming harder for people to find employment once they are let go.

Family Hack of the Week

This Skillet Cornbread courtesy of the Pioneer Woman makes for a delicious Thanksgiving side or breakfast treat.

Preheat oven to 450 degrees Fahrenheit. In a bowl, combine 1 cup yellow cornmeal, 1/2 cup all-purpose flour, 1 teaspoon salt and 1 tablespoon baking powder. In a measuring cup, add 1 cup buttermilk, 1/2 cup milk and 1 egg and stir together with a fork. Add 1/2 teaspoon baking soda and stir. Pour the milk mixture into the dry ingredients and stir until combined.

In a small bowl, melt 1/4 cup butter. Slowly add to the batter and stir until just combined. In an iron skillet, melt 2 tablespoons butter over medium heat. Pour batter into the hot skillet and spread to even out.

Cook on stovetop for 1 minute, then bake for 20 to 25 minutes until golden brown and edges are crispy.

What to Look for This Week

A few key reports will be released ahead of the Thanksgiving holiday. Tuesday brings an update on Existing Home Sales for October and the minutes from the Fed’s November 1 meeting. Look for the latest Jobless Claims on Wednesday.

Technical Picture

Mortgage Bonds ended last week trading in a range between support at the 101.035 Fibonacci level and a ceiling at 101.633. The 10-year remains above a key support level at 4.418%. If yields can move below this level, the next floor of support is the 100-day Moving Average at 4.32%.