Week of May 9, 2022 in Review

Inflation remains hot on both the consumer and wholesale levels. Here are the key stories to note:

Consumer Inflation Near 40-year Highs

What’s the bottom line? Not only does inflation lead to higher costs of goods, but it is also the arch enemy of fixed investments like Mortgage Bonds because it erodes the buying power of a Bond’s fixed rate of return. If inflation is rising, investors demand a rate of return to combat the faster pace of erosion due to inflation, causing interest rates to rise as we’ve seen this year.

In addition, within the report, rents rose 0.6% in April and increased 4.8% on a year over year basis. While this data has started to increase, the CPI report is still not capturing the double digit increases year over year that many other rent reports are showing.

Wholesale Inflation Remains Elevated

The Producer Price Index (PPI), which measures inflation on the wholesale level, rose 0.5% in April. On a year over year basis, PPI declined from 11.2% (which is the highest level on record since the methodology for collecting data was changed in 2010) to 11%. Core PPI, which also strips out food and energy prices, came in below expectations with a 0.4% increase in April. The year over year figure decreased from 9.6% to 8.8%.

What’s the bottom line? Producer inflation remains elevated, which often leads to hotter consumer inflation levels, as producers pass those higher costs along to consumers.

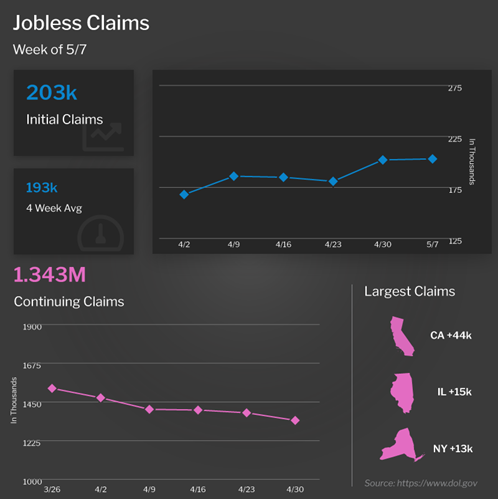

Initial Jobless Claims Rise for Second Straight Week

Initial Jobless Claims rose by 1,000 in the latest week, as the number of people filing for unemployment benefits for the first time was reported at 203,000. The previous week’s level was also revised higher by 2,000. Continuing Claims, which measure people who continue to receive benefits after their initial claim is filed, fell by 44,000 to 1.34 million. This is the lowest number of Continuing Claims since January 1970.

What’s the bottom line? Unemployment claims are extremely low and the labor market remains tight. But once we start to see claims pick up, especially initial claims, this could be a signal that the economy is slowing. Even though the latest increase in initial claims is minor, they have risen over the past two weeks. This is something we need to keep a close eye on as it’s an early indicator for the unemployment rate.

Small Business Expectations for Better Business Conditions Hits 48-year Low

April’s National Federation of Independent Business Small Business Optimism Index was unchanged from March, with the index overall remaining at its weakest level in two years. Inflation remains an issue for small business owners, with 32% reporting it’s their biggest problem at present. Though companies that expect higher selling prices fell 2 points to 70%, this follows the highest reading in the survey’s history of 72% in March.

What’s the bottom line? Owners expecting better business conditions over the next six months fell 1 point to a -50%, which is the lowest level in the 48-year history of the survey. Given that we have experienced several recessions, a housing bubble and the COVID pandemic over the last 50 years, the fact that owners are feeling so negative right now could be yet another indicator that we may be headed for a recession.

Also of note, the Cass Freight Index, which is a monthly measure of the North American freight market, was down 2.6% month over month in April and down 0.5% year over year. It’s possible that this reading includes some indirect impact from Chinese lockdowns, but we’ll likely see more of the direct impact in upcoming readings. Freight volume is an extremely reliable early-recession indicator, so it’s important to closely monitor future reports.

Fed Chair Jerome Powell Confirmed for Second Term

Fresh off the heels of being confirmed as Fed Chair for a second term in a 4 to 1 vote, Jerome Powell said in an interview with Marketplace that he couldn’t promise a “soft landing.” This means he can’t promise that the Fed can slowdown or tighten the economy in their attempt to bring inflation under control while avoiding a recession.

Powell said, “So it will be challenging, it won’t be easy. … Nonetheless, we think there are pathways … for us to get there.”

This is a big shift in tone from previous statements he’s made. Originally, Powell indicated that there’s a good chance to achieve a soft landing. He also previously considered inflation “transitory.”

Family Hack of the Week

This Friday, May 20 marks National Pick Strawberries Day. And whether you pick your own or purchase them, this recipe for Strawberry Muffins courtesy of the Food Network is sure to be a delicious treat.

Preheat oven to 375 degrees Fahrenheit. Line muffin tins with liners or spray with baking spray.

In a large bowl, stir together 3 cups all-purpose flour, 1 tablespoon baking powder, 1/2 teaspoon baking soda, 1/2 teaspoon Kosher salt and 1 1/2 teaspoons ground cinnamon. Make sure ingredients are combined well. In a 2-cup glass measuring dish, combine 1 1/4 cups milk, 2 extra large eggs (lightly beaten) and 2 sticks melted unsalted butter.

Make a well in the middle of the dry mixture and pour in the wet mixture, stirring until just combined. Add 2 cups diced fresh strawberries and 1 1/2 cups sugar and stir to gently combine.

Add batter to muffin tin and bake for 20 to 25 minutes until a cake tester comes out clean and tops are nicely browned.

What to Look for This Week

A plethora of housing reports will be released, beginning Tuesday when the National Association of Home Builders Housing Market Index will give us a read on builder confidence this month. April’s Housing Starts and Building Permits will be reported on Wednesday, while Existing Home Sales follows Thursday.

Also of note, we’ll get an update on regional manufacturing for New York via the Empire State Index on Monday and the Philadelphia Fed Index on Thursday. April’s Retail Sales data will be reported on Tuesday, while the latest Jobless Claims figures will be released on Thursday.

Technical Picture

Mortgage Bonds continue trading in the middle of a wide range, with a double ceiling of resistance comprised of the 101.656 level and the 25-day moving average, and the 0% Fibonacci level at 100.56 as support. The 10-year Treasury is still battling a ceiling at 2.92%. A bounce lower from this level could potentially be positive for Mortgage Bonds.