Week of March 6, 2023 in Review

- Pending Home Sales Rose for Second Straight Month

- Reports of a Housing Crash Not Supported by Appreciation Data

- What’s Really Going on With Jobs?

- Contraction in Manufacturing Continues

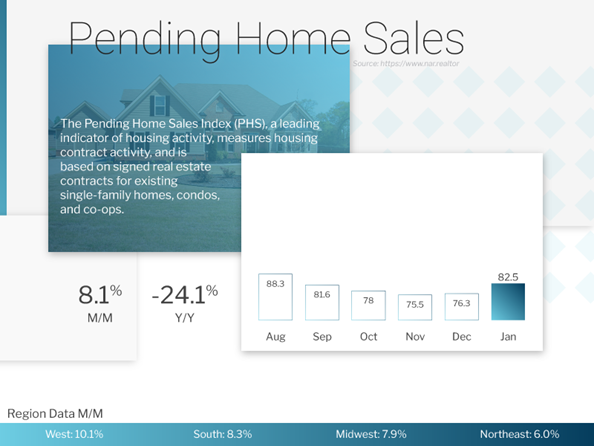

Pending Home Sales Rose for Second Straight Month

Pending Home Sales rose 8.1% from December to January, which was much stronger than expectations and follows the 1.1% gain in December. Sales were down 24.1% from a year earlier, though this was an improvement from the 33.9% annual decline in December’s report. Pending Home Sales is a critical report for taking the pulse of the housing market. It is considered a forward-looking indicator of homes sales because it measures signed contracts on existing homes, which represent around 90% of the market.

What’s the bottom line? While January is not known to be a strong housing month, this year it brought a considerable increase in activity as rates moved lower. Lawrence Yun, chief economist for the National Association of Realtors, confirmed, “Buyers responded to better affordability from falling mortgage rates in December and January.”

Rates did rise following the Jobs Report for January that was released on February 3, which was stronger than expected due in large part to seasonal adjustments made to the data. If upcoming economic data shows cooling inflation or weakness in the economy, the recent move higher in rates could reverse course. Expect another rebound in housing activity if this occurs.

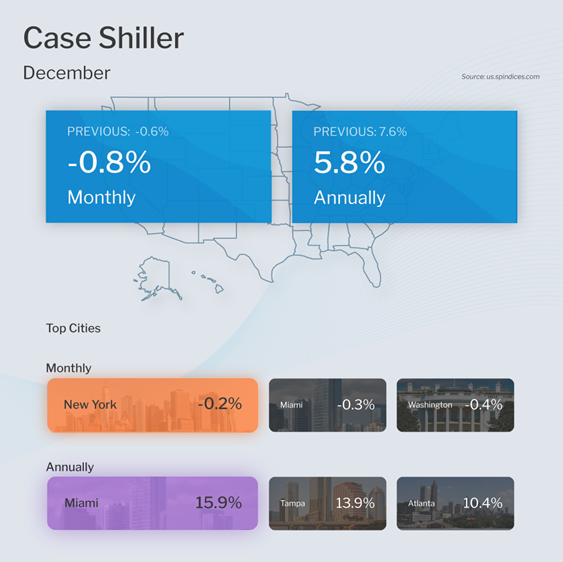

Reports of a Housing Crash Not Supported by Appreciation Data

The Case-Shiller Home Price Index, which is considered the “gold standard” for appreciation, showed home prices fell 0.8% from November to December but they were 5.8% higher when compared to December 2021. This annual reading is a decline from the 7.6% gain reported in November.

The Federal Housing Finance Agency (FHFA) also released their House Price Index, which revealed that home prices fell 0.1% from November to December. While prices rose 6.6% from December 2021 to December 2022, this was a decline from the 8.2% annual increase reported in November. FHFA’s report measures home price appreciation on single-family homes with conforming loan amounts, which means it most likely represents lower-priced homes. It also differs from Case-Shiller’s data, in that it does not include cash buyers or jumbo loans.

What’s the bottom line? Home prices have been softening nationwide, but S&P DJI Managing Director Craig J. Lazzara noted that they are only down 4.4% from their peak last June. This is a far cry from a housing crash of 20% that some in the media are predicting.

Plus, when important seasonal adjustments were made to Case-Shiller’s data, prices were only down 2.7% from the peak. These adjustments remove some of the market strength seen during the busier home shopping seasons and some of the weakness seen during the softer months, so we can see the true trend over time.

In addition, Case-Shiller’s 10-City and 20-City Indexes showed that prices in some major cities that were overheated are declining a bit more than they are in the nation overall. When removing those cities, prices around the rest of the country are flatter from the peak.

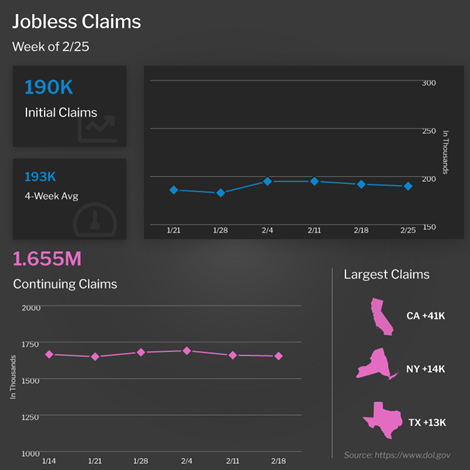

What’s Really Going on With Jobs?

Initial Jobless Claims declined by 2,000 in the latest week, as 190,000 people filed for unemployment benefits for the first time. Continuing Claims, which measure people who continue to receive benefits after their initial claim is filed, fell 5,000 to 1.655 million.

What’s the bottom line? Employers are clearly trying to keep the workers they currently have, as evidenced by the relatively low amount of Initial Jobless Claims we have been seeing each week. However, Continuing Claims data suggests it’s also harder for people who are let go to find new employment. While this number can be volatile from week to week, the overall trend has been higher, as Continuing Claims have risen by more than 300,000 since the low reached last September. This aligns with the decline in job postings that have been reported by sites like Indeed and ZipRecruiter.

Contraction in Manufacturing Continues

Economic activity in the manufacturing sector remained below 50 in contraction territory for the fourth straight month, as the ISM Index was reported at 47.7 for February. This data is compiled from a survey of purchasing and supply executives nationwide and measures the health of the manufacturing sector in the U.S. February’s reading was below expectations and follows important regional manufacturing indices, including those for the New York and Philadelphia regions, that also reported negative numbers last month.

Home Hack of the Week

Spring is nearly here, which means it’s important to schedule some seasonal maintenance on your home. Here are just a few items to tick off your list as the weather starts to warm.

Keep bugs away by making sure there aren’t any standing areas of water in your yard, which can be a breeding ground for mosquitoes and other pests. Also, if you notice any areas where water could pool, add soil to prevent both bugs and flooding.

Clear any debris from gutters and make sure none are loose or leaking. Also, double check that downspouts will drain away from your foundation, which is especially important if you’re in an area known for spring showers.

Make sure your screen doors and windows are free of any holes or tears. Also, check your outside faucets, hoses and sprinklers for frost damage to ensure they will work properly.

What to Look for This Week

Labor sector data will dominate this week’s headlines, starting Wednesday with ADP’s Employment Report, which will give us an update on private payrolls for February. The latest Jobless Claims data will be reported on Thursday while Friday brings the Bureau of Labor Statistics Jobs Report for February, which includes Non-farm Payrolls and the Unemployment Rate.

Also of note, Fed Chair Jerome Powell will be presenting the Fed’s Semiannual Monetary Policy Report to Congress next Tuesday and Wednesday. Investors will also be closely watching Wednesday’s 10-year Note and Thursday’s 30-year Bond auctions for the level of demand.

Technical Picture

Mortgage Bonds ended last week battling a ceiling at 99.547 and have formed a “morning star” pattern, which is a reliable indicator of a rebound. The 10-year moved sharply lower on Friday, breaking beneath the psychological 4% barrier.